← Resources

Pan American Auto Insurance

MidCandidate-ledOperational improvementProfitability

Case exhibits

5 exhibits for this case

PanAutoInsurance-exhibit-1

Suggested case structure

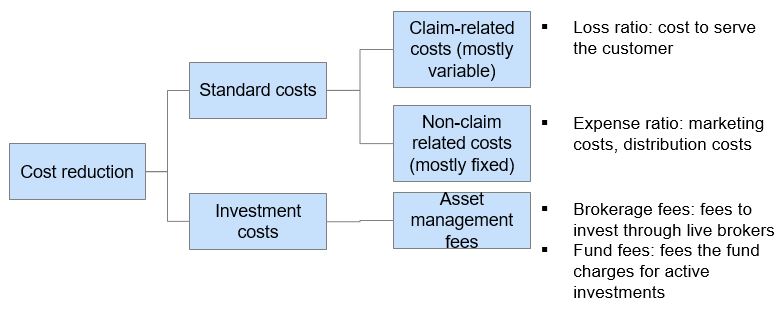

Key question: How can Pan improve margins by cutting costs?

Exhibit 1

Suggested steps ranked by priority:

- Claim-related/ variable costs- the interviewee should recognize that the loss ratio represents a large part of variable costs. Given the size of the loss ratio, this should be the first area of focus.

- Non-claim related/ fixed costs- the interviewee should recognize that fixed costs are largely represented in the expense ratio. Ideally, the interviewee will recognize the two large fixed costs mentioned in the prompt – marketing costs and distribution costs.

- Investment costs- The interviewee should recognize that asset management comes with additional fees, especially given the types of investments that Pan makes.

Make sure the interviewee builds a solid structure with at least two levels of logic. The interviewee may take a variable vs. fixed cost approach which is fine. If they do, guide them toward assuming variable costs are claim-related/ loss ratio costs and fixed is everything else. If they do not include investment costs, push them by asking if there are other areas of the business they should consider.

If needed, share Exhibit 1 with the interviewee

1. Claims-related costs

Let’s start by focusing on claim-related costs.

The interviewee should recognize that there are 2 ways to reduce claim-related costs.

- Tighter claims policy/pay fewer claims

- Attract safer drivers (who generate fewer claims)

Given that Pan is not willing to adjust its claims policy, the interviewee should focus on attracting safer drivers.

If the interviewee does not immediately eliminate “tighter claims policy” point them back toward the case prompt. Once focused on safer drivers, ask the interviewee what analysis they would do to determine opportunities for attracting safer drivers.

The interviewee should discuss the need to segment policyholders across several dimensions to determine if there are opportunities. Some dimensions that the interviewee may name: gender, age, geography, type of policy, tenure with Pan, etc.

The interviewee should also touch upon the metrics they would look at against these dimensions. The most direct metric would be loss ratio but the interviewee may also mention accident history, total claims filed or other metrics that would be indicators of driving safety.

Ensure the interviewee lays out a logical analysis to examine driver safety. If they’re unable to get there, push them along by asking them for what predictors may exist for a driver’s safety record that they could use when marketing to new customers. Once the interviewee has laid out a logical analysis, move on.

Share Exhibit 2 with the interviewee. Explain that it shows loss ratios cut across various dimensions. Explain that Pan has 3 main types of policies: standard auto insurance, commercial auto insurance (for business drivers, mostly truck drivers) and non-standard auto insurance (drivers who are considered risky by the insurance community – for Pan these are mostly drivers under 25)

Exhibit 2

Interviewee should recognize that loss ratios are comparable across every dimension except for age and policy type. Within those, there is likely overlap as the “Under 25” and “Non-standard” segments are leading to high loss ratios. Given the overlap, the interviewee should choose to focus on the non-standard segment going forward as it seems to be the most out-of-whack and is a superset of the “Under 25” segment.

Looking at this data, the interviewee may ask for the size of each segment as they may realize that they need more than just the loss ratio.

The non-standard segment accounts for ~20% of policies underwritten.

With this information, the interviewee should realize that the non-standard segment is a reasonably large share of the business and is bringing the loss ratio up. They should identify this as a segment that Pan likely wants to deprioritize and/or exit.

If interviewee chooses to focus on both “Under 25” and “Non-standard” push them to think about the overlap between the two and if one merits more focus for this initial exercise.

The interviewee may touch upon the risk of exiting the “Non-standard” market in the previous question. If they do not, push them on this topic ask them to think through what some of the key risks of deprioritizing/ cutting this set of customers might be

The interviewee does not have to hit these three risks on the nose. They may have others not on this list and may hit a subset. The key is that the interviewee is able to recognize that there may be non-economic reasons for targeting this market.

The interviewee should make a recommendation on how to move forward with this market. The decision will likely be one of three things:

- Continue to target the non-standard market with the same frequency – given the risks above, this market is important for the business to maintain

- Deprioritize the non-standard market – continue to serve this market but do not actively market to or target them. This may involve reducing them to 10-15% of the book of business.

- Exit the non-standard market – given the economics, some may reason that the risks are small and that it make s the most sense to exit the market entirely.

None of these are “right” and the key is that the interviewee consider both the upside and downside to working in this market.

2. Non-claims related costs

The interviewee should now move onto some of the non-claim related/ fixed costs. The interviewee has already laid out some of these costs. If the interviewee does not naturally focus in on one, ask them where they would start. The interviewee should recognize from the case prompt that marketing is a key budget item.

If the interviewee does not independently recognize the need to focus on marketing, push them by asking them to reread the case prompt.

The interviewee may have some thoughts around an analysis for marketing. They will likely ask for data around marketing expenses and where opportunity may lie.

Share Exhibit 3 with the interviewee. It includes recent year data for spend on marketing and the number of customers that were acquired through that channel.

Exhibit 3

The interviewee should be able to look at this data and see that they can easily calculate a cost per acquisition as a way of calculating ROI.

The interviewee should be able to calculate the table above. If the interviewee is unable to get to a CPA analysis, push them there by having them think through a “value for the dollar”.

Exhibit 4

If needed, share Exhibit 4 with the interviewee

In constructing the CPA table, they should find that the CPA for TV is $15 vs. $2 and $1 for Digital and Referral. The interviewee should make a recommendation to shift marketing dollars toward the most cost efficient channels as a means of saving money. The interviewee should acknowledge the limitations of the analysis which include the fact that marketing ROI tracking is often hard and imprecise (e.g., people may see the brand on TV but sign up for a policy via digital channels) and that we may be “skimming” customers through the digital and referral channels since the spend is low (meaning we may be selectively pulling in the heaviest users/ lowest cost customers in those channels and as we expand budget, those channels will be come less efficient). The analysis also does not speak to the profitability of customers by channel, which may vary and may be skewed.

If the interviewee does not get to the CPA analysis, push them there by asking questions about how they would measure efficiency. If the interviewee does not address risks, ask them if they think there are shortcomings or risks with the analysis.

The interviewee should recognize that there was one other major non-claim related cost mentioned in the case prompt – distribution costs.

If the interviewee does not independently recognize the need to focus on distribution costs, push them by asking them to reread the case prompt.

The interviewee may have some initial thoughts on how to reduce these costs. The interviewee should ask for data around the size of these costs and how much of total costs they represent.

Share Exhibit 5 with the interviewee. Mention that distribution costs are about 40% of total non-claim related costs (~11% of revenue – 28% expense ratio * 40%). iSurance is an online direct-to-consumer insurance provider and generates comparable revenue as Pan.

Exhibit 5

The interviewee should now recognize that agency commissions represent the largest opportunity for Pan as they are the largest part of distribution costs and a significantly higher cost than at iSurance. The interviewee should recognize that iSurance distributes direct-to-consumer and is able to save on agency commissions in this way. The interviewee should brainstorm how Pan can mimic this strategy. Pan can start a hotline to sell insurance by phone or Pan can distribute policies over the internet. The interviewee should also acknowledge the risk that this would be a new business for Pan and they may not have the expertise to enter this new model in a cost effective way. Finally, the interviewee should be able to size the opportunity here. For example, if Pan can close the gap 50% between them and iSurance, they would save $23.75M (but would likely see an increase in customer communication costs and potentially after sales customer service).

3. Investment related costs

Finally, the interviewee should move forward to investment related fees. Based on the case prompt, the interviewee should recognize that there are two major types of costs that Pan is paying – brokerage fees and fund fees (for the active funds).

The interviewee should acknowledge the ways to reduce these costs. In order to reduce brokerage fees, Pan can either bring brokerage in-house or can work through cheaper channels (e.g., online, telephone brokerages).

In order to reduce the fund fees, Pan can invest in lower cost passive investment funds. The interviewee should recognize the tradeoff here – active funds typically show better returns but are also more volatile. The interviewee should acknowledge that shifting to more passively managed funds would result in a shift in strategy and so it needs to be well thought out.

The interviewee may have other thoughts on reducing investment related costs. For instance, by consolidating investments into fewer vehicles. These show that the interviewee is thinking beyond the clues given in the case.

4. Summary and final recommendation

The interviewee should now move onto to making a final recommendation to Pan on how to improve margins in a saturated market.

If the interviewee does not begin to summarize the findings from the case, push them there by simulating a situation where the interviewee runs into the head client who asks for a recap of the team’s work.

The interviewee should summarize the case including the following facts:

- Pan can effectively reduce both claims-related and non-claim related costs

- Pan can reduce claims-related costs by deprioritizing some of the more costly segments of the market, like the non-standard segment

- Pan can reduce non claims-related costs by

- Investing in more productive marketing channels like digital and referral marketing

- Shifting distribution from agents to direct-to-consumer channels as hotline or online policy distribution

- Investing in less costly brokerage channels (telesales or online) or more passive funds

- Each of the above actions comes with a risk that should be carefully assessed