Hospital

Case exhibits

1 exhibit for this case

Hospital-exhibit-1

Suggested case structure

- Revenue Analysis: Understand the driver of revenue and see if any factors have changed in the past one year

- Cost Analysis: Understand the drivers of cost to get to the root cause of the loss

- Possible solutions: Based on the root cause, recommend steps to move towards break-even

1. Revenue Analysis

Allow the interviewee to ask for more information about revenue drivers and then share the information below.

If the interviewee starts with the cost analysis, then move to that section and share the background information about the cost.

Share the below information verbally when requested by the interviewee.

- The insurers drive almost all of the revenue of the hospital.

- The revenue is fixed on the basis of managed care contracts with insurers. These contracts are signed for a period of 3 years and are non-negotiable.

- The hospital signed the contract with the insurers at the beginning of this financial year.

- The hospital made an aggressive bid in order to secure those contracts.

- Although, the patient volumes have remained largely at the same level as last year, the revenues have dropped by 20% this year.

The interviewee should note that the aggressive pricing used to bid for the contract could potentially be one of the reasons for the loss this year. However, the costs still need to be examined.

2. Cost Analysis

Share the below information verbally when requested by the interviewee.

- The hospital has fixed costs which cannot be altered – these are largely related to building and equipment maintenance etc.

- Employee costs are the biggest cost head under variable costs.

- The client has already indicated that it would not be laying off staff in order to reduce costs

- The second largest cost component under variable costs is resource utilisation by the medical personnel. This includes materials, medications, disposables etc.

- The finance team has estimated that the resource utilisation is 15% higher than what was envisaged during the contract negotiated.

- Some of the overhead costs are not fixed and can be optimised.

Key insight

The hospital had bid aggressively to secure the contract. The resource utilization is higher than what was envisaged in the contract.

Hence, the revenue from the insurer is not sufficient to cover the actual costs. Since, payroll costs cannot be reduced, the hospital would need to look at optimizing resource utilization.

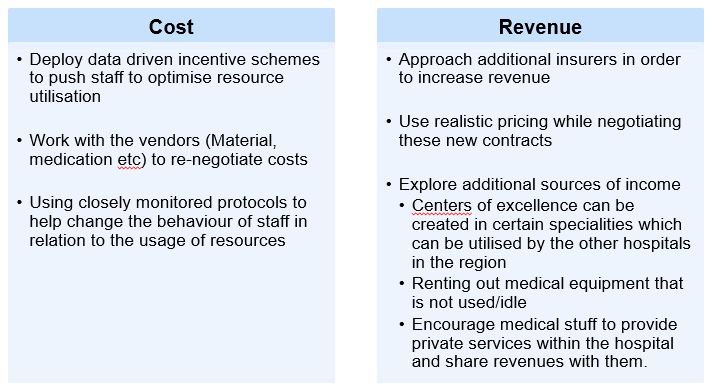

3. Final recommendation

After the interviewee has exhausted his options, share that this was an actual situation with a client and share the recommendations of the consultants who worked on the case.

Exhibit 1