Credit Francais

Case exhibits

3 exhibits for this case

CreditFrancais-exhibit-1

Suggested case structure

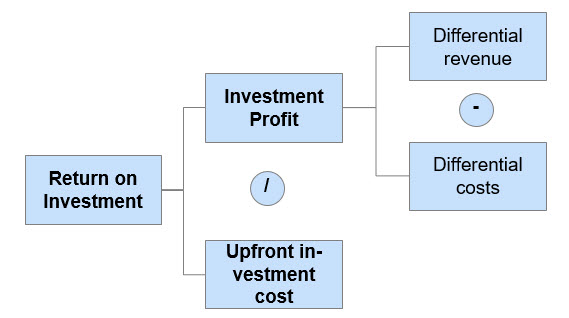

- Return on investment: Firstly, the interviewee should inquire whether the decision is made on budget constraints and should understand that the key parameter to be evaluated is the return on investment

- Profitability analysis: Secondly, the interviewee should inquire about the differential revenue and the differential costs generated by the two initiatives, in order to estimate the differential profits for each of the two options

- Other factors: The interviewee should qualitatively discuss other factors that must be taken in consideration when evaluating the two options

1. Profitability Analysis

This part of the case should be led by the interviewer, introducing the interviewee to the fundamentals of the banking sector.

- Banks’ revenue can be divided into two broad categories

- Interest revenues, which are revenues deriving from lending money to customers at an interest rate that is higher with respect to the one that the bank pays on the money it borrows; these revenues may usually be computed as the outstanding loans times the interest rate

- Commissions and fees, which are revenues deriving either from banking transactions (e.g., wire transfers, credit cards, etc.) or from investment products (e.g., funds, portfolio management, etc.)

- Banks’ costs may also be divided into two broad categories:

- Administrative and operating costs, which are costs necessary to sustain the banks’ regular activity, including personnel costs

- Credit cost, which is the cost related to defaults on loans; this is usually computed as cost of risk, expressed in basis points, times the outstanding loans

- Cost of funding, which is the interest rate the bank pays on the money it borrows. For simplicity, this can be assumed to be zero throughout the case

At this point, brainstorm with the interviewee the sources of revenue and costs for both the initiatives:

- Expanding into the consumer credit market generates interest revenue, while there will be both some administrative costs for the employees and credit costs due to defaults on loans;

- Increasing penetration of asset management products will generate commission and fees, while there will be some costs for additional personnel;

- Both initiatives will require an upfront investment cost, mainly related to the marketing of the new product and the setup of the units.

a. Consumer credit market

b. Asset management products

The additional revenue for each client category may be computed as follows:

(𝐴𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑟𝑒𝑣𝑒𝑛𝑢𝑒=𝑁𝑜.# 𝑜𝑓 𝑐𝑙𝑖𝑒𝑛𝑡𝑠∗𝐶𝑎𝑚𝑝𝑎𝑖𝑔𝑛 𝑃𝑒𝑛𝑒𝑡𝑟𝑎𝑡𝑖𝑜𝑛∗𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑎𝑠𝑠𝑒𝑡𝑠∗(𝐹𝑢𝑡𝑢𝑟𝑒 𝑟𝑒𝑣𝑒𝑛𝑢𝑒−𝑐𝑢𝑟𝑟𝑒𝑛𝑡 𝑟𝑒𝑣𝑒𝑛𝑢𝑒) )

Thus:

𝑃𝑟𝑖𝑣𝑎𝑡𝑒 𝑟𝑒𝑣𝑒𝑛𝑢𝑒=20,000∗20%∗500,000∗(0.8% −0.2%)=12 𝐸𝑈𝑅 𝑚𝑖𝑙𝑙𝑖𝑜𝑛

𝐴𝑓𝑓𝑙𝑢𝑒𝑛𝑡 𝑟𝑒𝑣𝑒𝑛𝑢𝑒=100,000∗10%∗200,000∗(0.5% −0.15%)=7 𝐸𝑈𝑅 𝑚𝑖𝑙𝑙𝑖𝑜𝑛

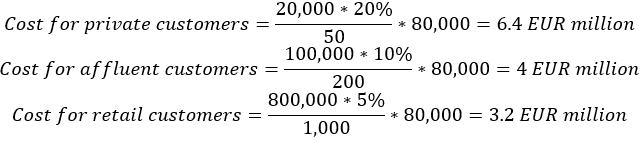

𝑅𝑒𝑡𝑎𝑖𝑙 𝑟𝑒𝑣𝑒𝑛𝑢𝑒=800,000∗5%∗80,000∗(0.3% −0.1%)=6.4 𝐸𝑈𝑅 𝑚𝑖𝑙𝑙𝑖𝑜𝑛

Total revenue is thus:

𝐴𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑟𝑒𝑣𝑒𝑛𝑢𝑒=𝑃𝑟𝑖𝑣𝑎𝑡𝑒 𝑟𝑒𝑣.+𝐴𝑓𝑓𝑙𝑢𝑒𝑛𝑡 𝑟𝑒𝑣.+𝑅𝑒𝑡𝑎𝑖𝑙 𝑟𝑒𝑣.=12+7+6.4=25.4 𝐸𝑈𝑅 𝑚𝑖𝑙𝑙𝑖𝑜𝑛

The employee cost for a particular segment may thus be computed as:

Thus:

Total yearly costs and profits for the asset management initiative are thus:

𝑇𝑜𝑡𝑎𝑙 𝑎𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑐𝑜𝑠𝑡𝑠=6.4+4+3.2=13.6 𝐸𝑈𝑅 𝑚𝑖𝑙𝑙𝑖𝑜𝑛

𝑇𝑜𝑡𝑎𝑙 𝑝𝑟𝑜𝑓𝑖𝑡=𝑇𝑜𝑡𝑎𝑙 𝑎𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑟𝑒𝑣𝑒𝑛𝑢𝑒𝑠 −𝑇𝑜𝑡𝑎𝑙 𝑎𝑑𝑑𝑖𝑡𝑖𝑜𝑛𝑎𝑙 𝑐𝑜𝑠𝑡𝑠=25.4−13.6=11.8 𝐸𝑈𝑅 𝑚𝑖𝑙𝑙𝑖𝑜𝑛

2. Return on investment

Upfront investment costs are:

- 30 EUR million for the consumer credit initiative

- 8 EUR million for the asset management initiative

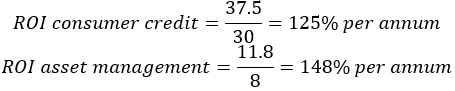

The ROI, measured in annual profit divided by investment (neglecting discount rates) is thus:

As we have budget constraints, investments should be ranked from the highest ROI to the lowest ROI. Thus, the company should pursue the asset management initiative and use the remaining money of the “special projects” budget for the alternative investment yielding a 130% per annum ROI.

3. Discussion

A deeper analysis shows that each of the initiatives is actually made up by three “lower-level” initiatives, which could be carried out on a stand-alone point of view. Thus, the previous solution is not necessarily the one that will generate the highest ROI, because it has been identified by examining only two sets of possible initiatives. A more thorough analysis would thus require to compute the additional profits of each of the six initiatives, ask the interviewer to split the upfront investment costs into costs for each one of the initiatives and compute the ROI of each initiative. Then, initiatives would be ranked from the one with highest ROI to the one with lowest ROI (including the alternative investment) and would be chosen in order up to the cap of the “special projects” budget.

Summary:

Given our budget constraints and the alternative investments available, we recommend choosing the asset management initiative as it yields the highest ROI. The consumer credit initiative yields an higher yearly profit compared to the asset management initiative (37.5 vs. 11.8 EUR million), but, considering investment cost, has lower ROI (125% per annum vs. 148% per annum).

4. Other factors

- Revenue increase:

- Strategic fit: Which qualitative factors would you consider in the decision (e.g., fit with the bank’s core business, easiness of finding adequate resources, etc.)?

- Regulation: How do you think regulatory issues should be taken in consideration in making the decision?

- Long-term scenario opportunities: Which one do you think is a better investment in the long-term: consumer lending or investment products? Which are the macro-economic variables that would influence this choice?

- ROI discount rate: ROI has been computed without discounting future cash flows: how would this influence the decision?